Report: Regional Office Market – Office Market in Regional Cities in Poland 2024 summary & forecasts for 2025 – report by AXI IMMO

Developers exercise caution in new investments

AXI IMMO, Poland’s largest commercial real estate firm, presents the “Office Market in Regional Cities” report, summarising the situation in Poland’s eight largest regional office markets.

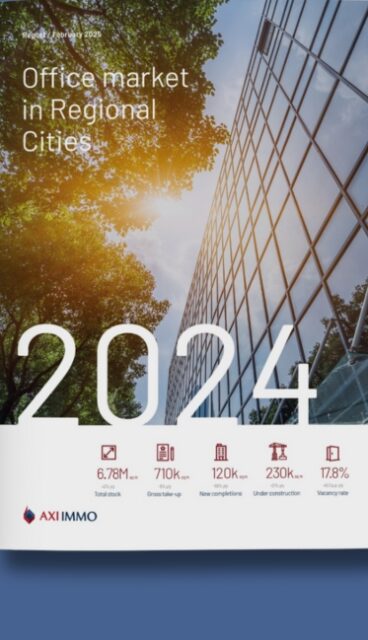

The regional office market in Poland (Kraków, Wrocław, Tricity, Katowice, Łódź, Poznań, Szczecin, and Lublin) is adapting to evolving conditions. The high availability of office space (an average of 17.8%) prompts tenants to take up greater flexibility in lease negotiations, while developers are reducing their activity (120,000 sq m of new supply delivered in 2024). Despite challenges in gross take-up (710,000 sq m, -5% y/y), stabilisation is observed, with office building owners focusing on improving building standards and introducing flexible leasing models.

Office Market in Regional Cities – Supply Slowdown – Developers Acting with Caution

The total modern office space in regional cities currently amounts to 6.78 million sq m (+2% y/y). However, the scale of new investments is declining – in 2024, only 120,000 sq m was delivered to the market (-56% y/y). Kraków, Wrocław, and Tricity remain the largest regional markets, holding respective shares of 27%, 20%, and 16% of total regional office stock. Among the largest completed projects were investments by Cavatina – Grundmana Office Park A in Katowice (20,700 sq m) and Quorum Office Park A in Wrocław (18,200 sq m). Vastint also delivered the B10 office building in Wrocław (14,100 sq m). Currently, 230,000 sq m of office space is under construction, with Kraków and Poznań leading activity. The largest projects under construction include AND2 in Poznań (40,000 sq m, Von der Heyden Group) and Tischnera Green Park 1 in Kraków (24,000 sq m, Stalprodukt). The high level of unoccupied space is causing developers to proceed cautiously. The average vacancy rate in regional cities stands at 17.8% (+0.3 pp y/y), with the highest vacancy rate in Katowice (23.2%) and the lowest in Szczecin (7.7%).

Emilia Trofimiuk, Research Manager, Research Department, AXI IMMO Group, explains:

“Decisions to launch new investments are being made with great caution. A crucial factor will be securing pre-leases at the preparation stage – before a project enters the execution phase, owners will aim to ensure a stable occupancy level. Meanwhile, the high availability of office space benefits tenants, increasing their negotiating power. Building owners are adapting their offerings, proposing more competitive lease terms, and investing in modernisation and additional amenities for tenants.”

Take-up – Lease Renewals as the Key Trend

In 2024, tenant activity in regional cities amounted to 710,000 sq m (-5% y/y). The transaction structure shows a significant increase in the share of renegotiations and lease renewals (51%) at the expense of new leases (41%). The highest leasing activity was recorded in Kraków, Wrocław, and Tricity, accounting for 37%, 21%, and 16% of total regional take-up. These are also the cities with the largest office stock. Subleasing remains a popular trend, enabling companies to optimise rental costs. The IT and business services sectors continue to dominate tenant take-up. Volvo Tech Hub was the largest new lease transaction in 2024 in regional cities, leasing 10,100 sq m in Brain Park C in Kraków.

Stable Rents, Rising Service Charges

Asking rents in most office buildings in regional cities remain stable, ranging from EUR 9.00 to EUR 17.80 per sq m per month, with the highest rates observed in Kraków and Poznań. However, service charges have increased and range from PLN 9.00 to PLN 36.80 per sq m per month. The rising service charge costs stem from increasing building maintenance and energy expenses.

Monika Rykowska, Head of Research, AXI IMMO Group, summarises:

“Forecasts for 2025 indicate moderate developer activity, approx. 160,000 sq m of new office space will be delivered to regional markets. Decisions on further investments will depend on pre-lease levels and market demand. On the take-up side, we expect tenants to continue optimising their occupied space while maintaining high office fit-out and design standards. The importance of flexible formats is also growing – both in the co-working model and serviced offices managed by external operators or building owners.”

About AXI IMMO

AXI IMMO offers comprehensive advisory services related to commercial real estate, including warehouse and office leasing and property management, real estate valuation, land acquisition, and sales. The firm also offers B2B and B2C supply chain management services. AXI IMMO’s greatest advantage is combining international business standards with deep local market knowledge. AXI IMMO has received numerous awards, including Best Local Agency of the Year in 2012 – 2019 and 2021 in the CiJ Awards and the award for Best Team in the warehouse sector in 2016 – 2017. In 2019 and 2023, the firm was the winner in the Local Agency category, and in 2024 it was named Advisor of the Year at the CEE Investment Awards. AXI IMMO was named Local Agent of the Year in 2023 and 2024 in the CEE region at the CEEQA awards. The firm’s most recent achievement is the title of Advisor of the Year in the Prime Property Prize 2024.

Report — Office Market in Regional Cities Poland 2024 summary & Forecasts for 2025

Fill in the form and receive a link to the report in your email inbox

Recent articles

31 March 2026

Serviced Offices – When This Leasing Model Truly Makes Sense

Thinking about a new office? This guide breaks down the differences between a serviced office and a traditional one to help you find the most cost-effective option for your business.

30 March 2026

AXI IMMO advises Bel-Pol on a 5,600 sq m warehouse lease at Panattoni Park Warsaw North III, Poland, March 2026

Bel-Pol secures modern logistics and warehouse space in the north-eastern Warsaw agglomeration.

25 March 2026

AXI IMMO Report: Analysis of the Warehouse & Industrial Sector in the Łódź Voivodeship, Central Poland

Łódź's Logistics Sector Booms, Reaching 1.17 Million Sqm in Tenant Demand!

24 March 2026

10000 sq warehouse space for TVM Group in Poland, AXI IMMO Advices

TVM Group was supported throughout the property selection process and lease negotiations by AXI IMMO.